How to build – and defend – a franchise in US energy finance

Credit Suisse/UBS and FCB/SVB: Two distressed banking mergers and what they mean for the US power market.

The last two weeks in financial markets have not quite rivalled the rollercoaster weeks of September 2008, but they have come close. Now, with March 2023 coming to an end, two mergers give the market a chance to look at how US power finance is evolving.

The first of the two mergers was by far the larger – at least in terms of assets. On 19 March, the Swiss Financial Market Supervisory Authority brokered the acquisition of ailing Credit Suisse by its rival UBS. Then on 26 March, First Citizens Bank, which had owned CIT since January 2022, agreed to buy Silicon Valley Bank, essentially by agreeing to share losses on its $110 billion portfolio with the Federal Deposit Insurance Corporation.

The all-share UBS acquisition in theory valued Credit Suisse’s equity at CHF3 billion ($3.3 billion), but the deal wiped out the holders of Credit Suisse’s subordinated regulatory capital, to the sounds of wailing and gnashing across European debt capital markets. The equity value was a pittance next to the $575 billion in assets that Credit Suisse had on its balance sheet – or the $1.1 trillion of UBS assets. UBS was anxious to point to the CHF25 billion in downside protection it had been offered, as well as unlimited access to liquidity facilities at the Swiss National Bank.

It also noted that the combined business should be able to “generate annual run-rate of cost reductions of more than $8 billion by 2027”. That figure has led to some speculation about where potential cuts to banking headcount might fall. With Goldman Sachs promising 3,200 cuts in February, and Morgan Stanley 1,600 losses in December 2022, the 2023 investment banking job market is looking decidedly sickly.

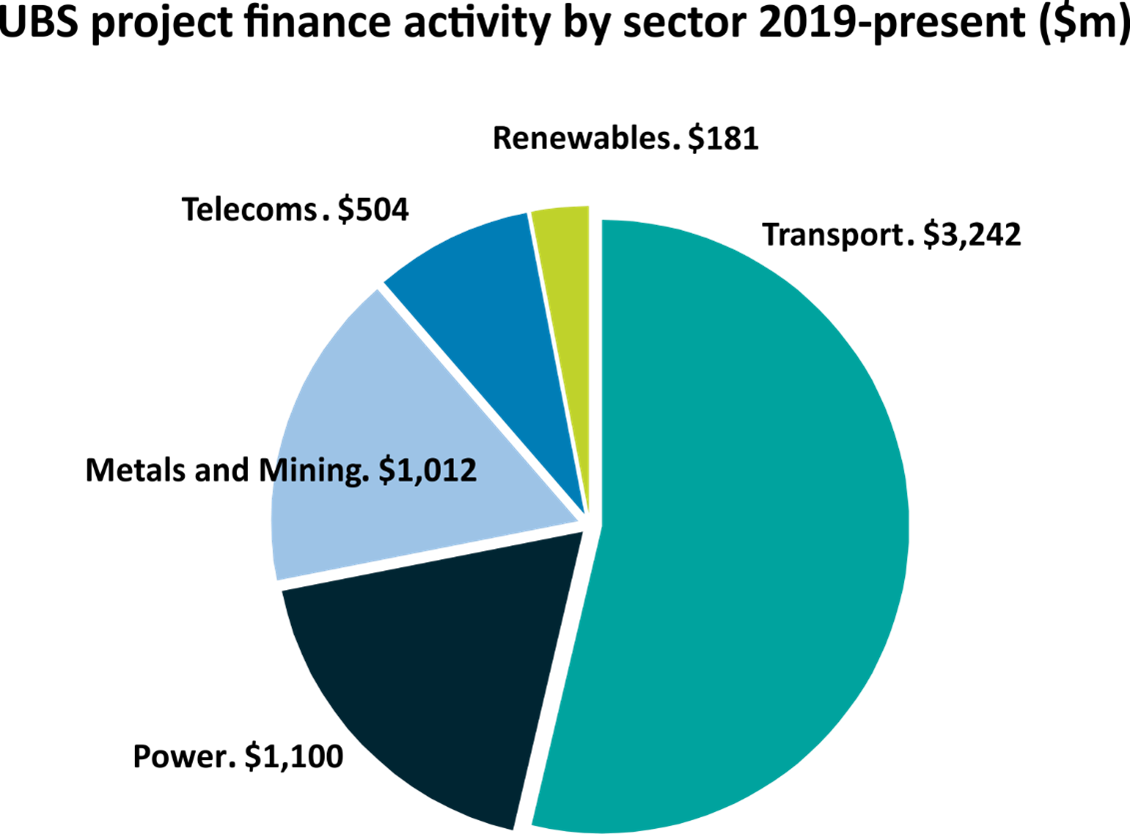

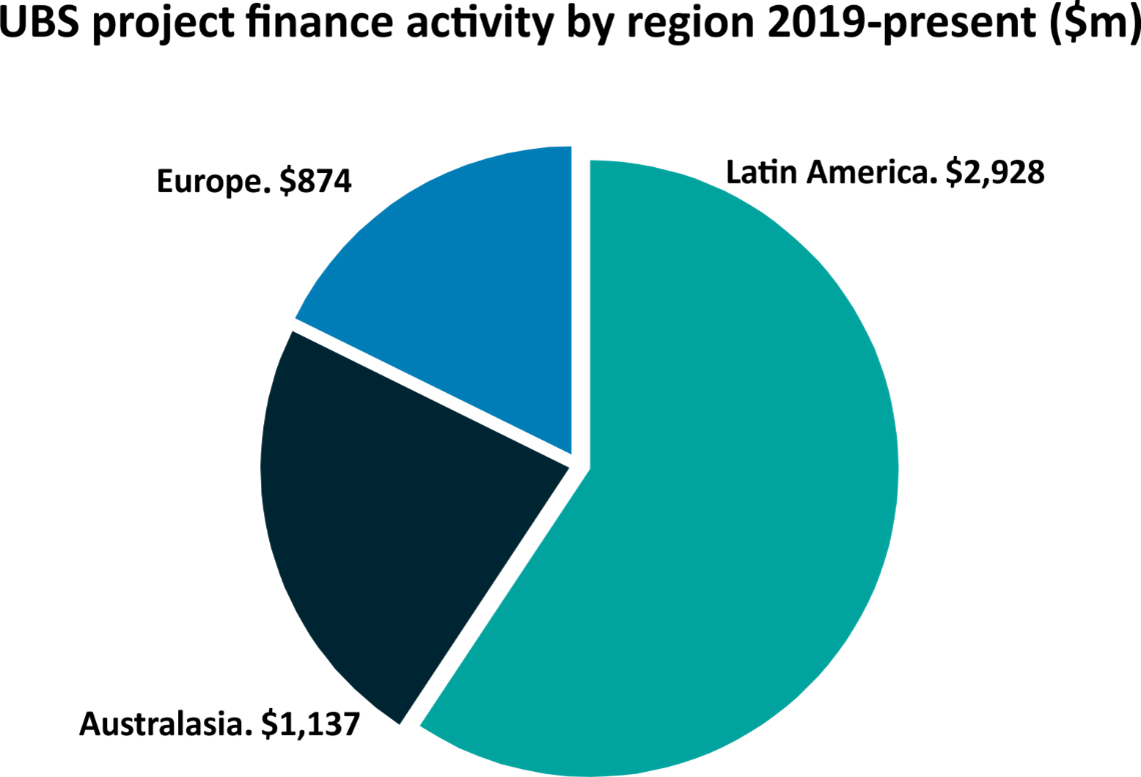

In Proximo’s corner of financial markets, the news is likely to be reasonably positive, assuming UBS wants to stay in the project finance business at all. According to Proximo Intelligence’s data, UBS helped mobilise approximately $6 billion in project finance volumes from the start of 2019 to the present, for a total of 14 transactions.

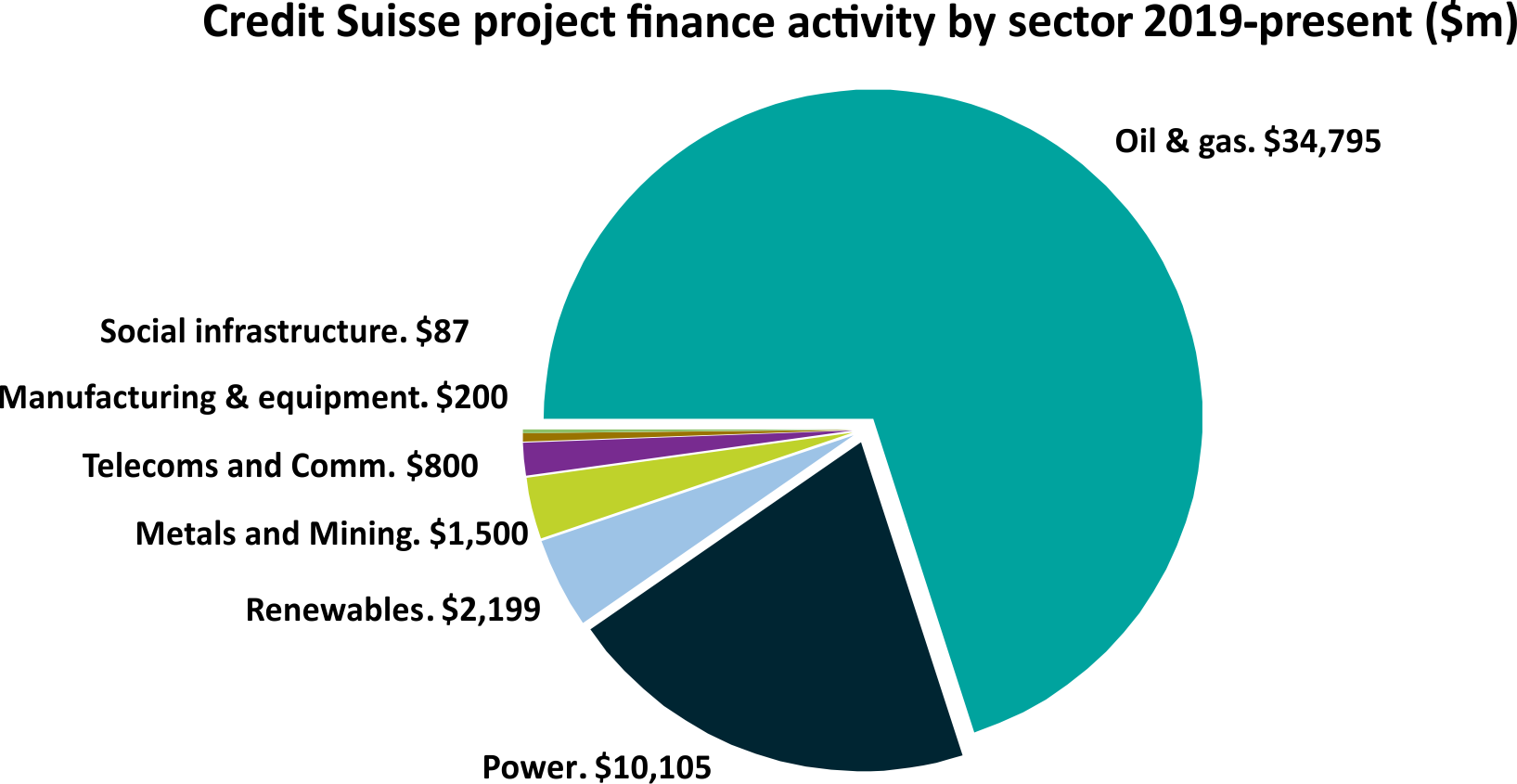

Source: Proximo Intelligence

That small transaction record is fairly well spread, with very slightly under half its activity in Latin America, slightly over a third in Asia-Pacific, and less than a sixth in Europe. UBS had a reputation as an effective bookrunner of emerging markets project bonds, particularly local currency debt in Brazil. In large part because of that Brazilian debt franchise, transport accounts for nearly half of that activity.

Source: Proximo Intelligence

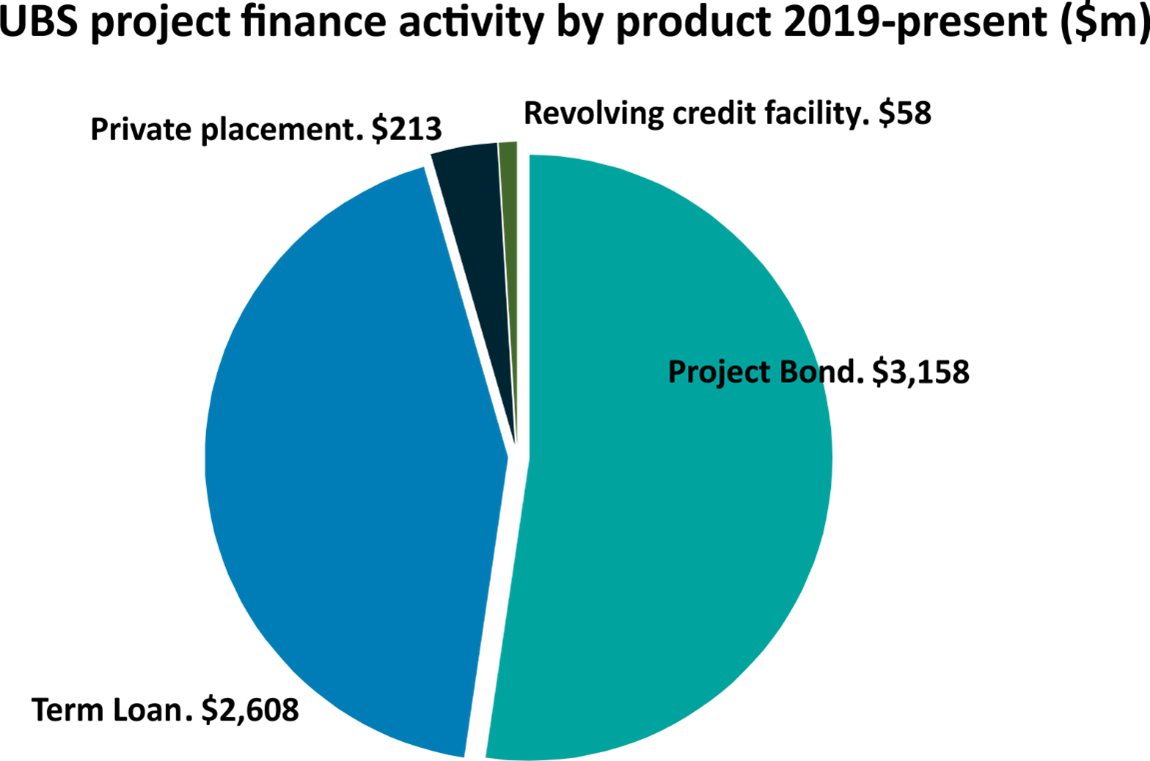

By tranche type, bonds and private placements predominate, with just four term loan transactions – a BRL loan for an AES portfolio, the $1 billion Sierra Gorda copper mine bank financing, the $1.65 billion equivalent refinancing of Melbourne’s West Gate Tunnel, and InfraVia’s Swiss data centre transaction.

The overlap with Credit Suisse’s activity is extremely small, comprising the InfraVia data portfolio, the bond refinancing of San Miguel’s Ilijan CCGT, and a bond financing for Adani’s Transmission lines, though given Adani’s own struggles in 2023, that synergy is perhaps best glossed over.

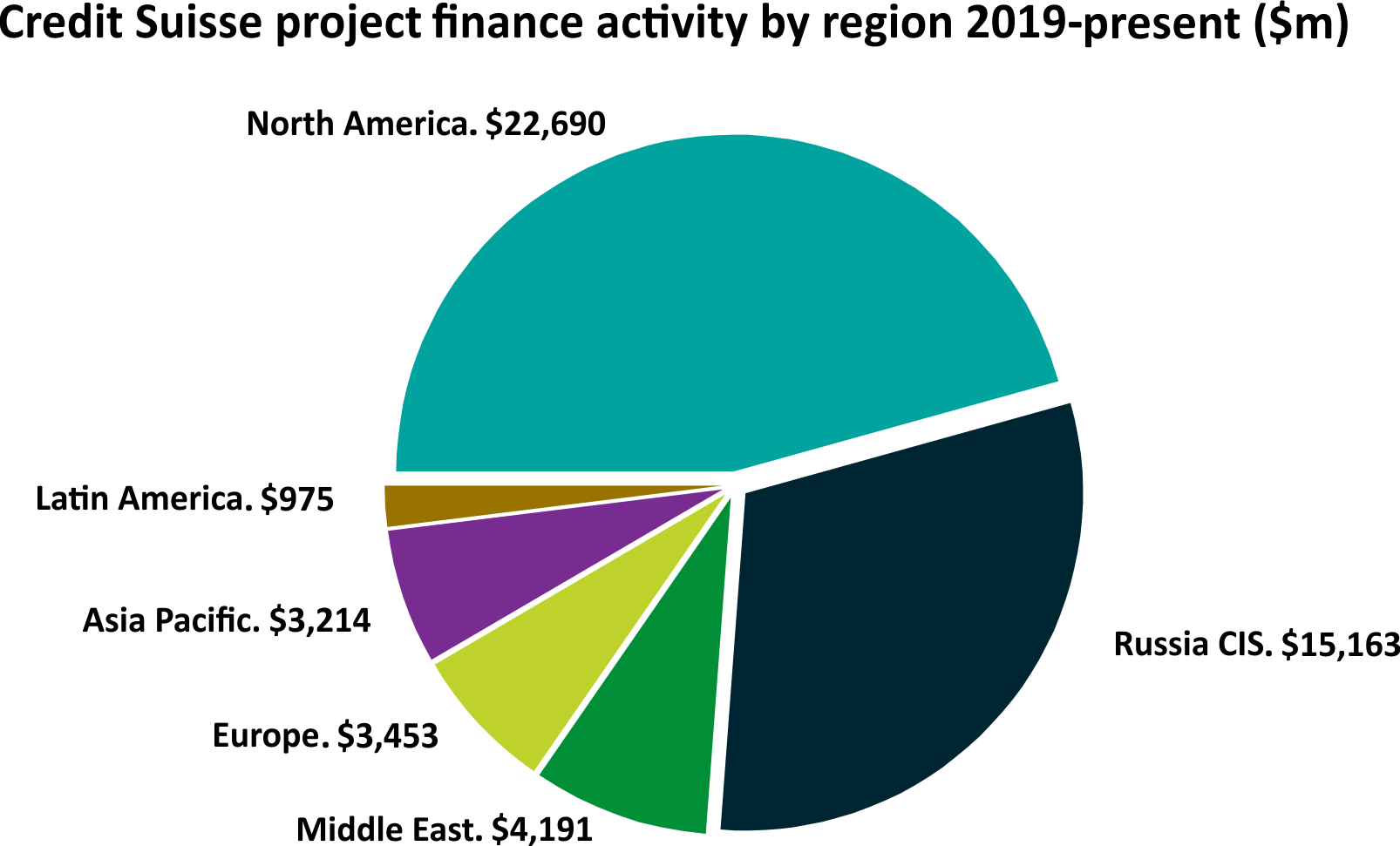

But Credit Suisse is much more of a project finance powerhouse, mobilising just under $50 billion in deal volume since the start of 2019. One deal – the $12.8 billion export financing for Gazprom’s Amur gas processing plant – accounts for a good deal of that volume, but even without it, Credit Suisse was a real force in energy finance.

About $24 billion of its activity comprised uncovered term loans, and another $10 billion project bonds, and another $12 billion ECA and DFI-related financings. Oil & gas and power dominate transaction volumes, though activity is spread much more evenly across regions.

Source: Proximo Intelligence

Source: Proximo Intelligence

Credit Suisse has enjoyed a 25-year run as a pioneer of new methods of financing and distributing infrastructure assets. It surfed the wave of the US merchant power boom around the turn of the century, surviving the fall-out and having a successful second act by shifting the focus of US power finance from the bank market to the term B leverage loan market. It educated these investors on construction and offtake risk, and both its competitors and smaller niche banks have benefited as a result.

Credit Suisse also probably did more than any other bank to develop the project bond market, taking what was initially a niche private placement-type take-out option for small independent power producers and putting together large and well-distributed issues for generation portfolios and large midstream and upstream oil and gas operators, in both developed markets. Adebayo Ogunlesi, who led this effort, became head of Credit Suisse’s global investment bank in 2002, probably the most successful project finance banker yet.

The bank’s project finance client list is long and illustrious, including ArcLight, BlackRock, Brookfield, Cheniere and LS Power. Its alumni have appeared at Bank of America and Barclays, but in particular at Global Infrastructure Partners, the infrastructure fund powerhouse that Ogunlesi formed in 2006 and continues to lead, and which benefited from some original support from Credit Suisse and GE. GIP now dwarfs the in-house infrastructure asset management businesses that UBS and Credit Suisse have since developed.

Both Credit Suisse and UBS are weak in renewables project finance, and if UBS management is serious about continuing with the product and burnishing its ESG credentials then it will need to retain some Credit Suisse personnel and point them at the US independent power producers and funds that are most active in the sector. A focus on domestic Swiss business would not require a project finance team of any size or note.

The First Citizens/SVB merger is probably going to be more immediately consequential for the US power market. CIT, which merged into FCB in 2022, had as long a history of structurally innovative US power financings as Credit Suisse, as well as being a pioneer in leveraged leasing, Canadian PPP and Israeli infrastructure, among other sectors, though in recent years it was best known as an arranger of bank financings for North American energy and infrastructure assets.

Proximo looked at the SVB project finance book earlier this month, and it showed some decided concentrations by assets and sponsors. A combined SVB/CIT entity would not gain a great deal in geographical diversity, but it would have a much wider spread of assets. Renewables would predominate, but oil & gas, conventional power and digital infrastructure would also be sizeable business lines.

Source: Proximo Intelligence

First Citizens did not mention the CIT franchise when announcing its acquisition of the SVB business. That is perhaps unsurprising, given that project finance did not amount to a particularly large chunk of either entity’s book. SVB is still generally viewed as a banker to the tech sector, and the clean tech clients that evolved into project finance sponsors are rather overshadowed by the corporate banking it did for big venture capital firms and their portfolio companies.

But depending on how the merger shakes out, the combined FCB/SVB operations could become a top-tier force in US power finance – a $32 billion aggregate book definitely allows for entry to that circle. And whereas both UBS and Credit Suisse were better known as advisory and capital markets firms (in the moving business rather than the storage business), a First Citizens-led project finance group would hopefully constitute a stable and reliable source of term and revolving debt to the renewable energy sector – just what the sector’s sponsors need right now.