US renewables’ wait for the IRA to kick in

The package of incentives in the 2022 Inflation Reduction Act should help maintain US leadership in clean energy development and financing. But, according to Proximo Intelligence’s data, the effects have yet to be fully felt.

The US has long been a pioneer in developing and financing sustainable energy sources, even as it becomes an increasingly influential exporter of oil and natural gas. Its long experience of project financing power assets, and liquid capital markets, make it by far the largest single market for power finance, rivalling even Europe’s aggregated volumes.

Now the Biden administration is embracing a multifaceted approach that combines a rapid expansion in renewable energy development, a decreasing dependence on fossil fuels (at least domestically), and faster adoption of technologies that will reshape patterns of energy production and consumption. The US has made remarkable strides in the last five years in increasing financing volumes, but the impact of recent legislation is so far less clear.

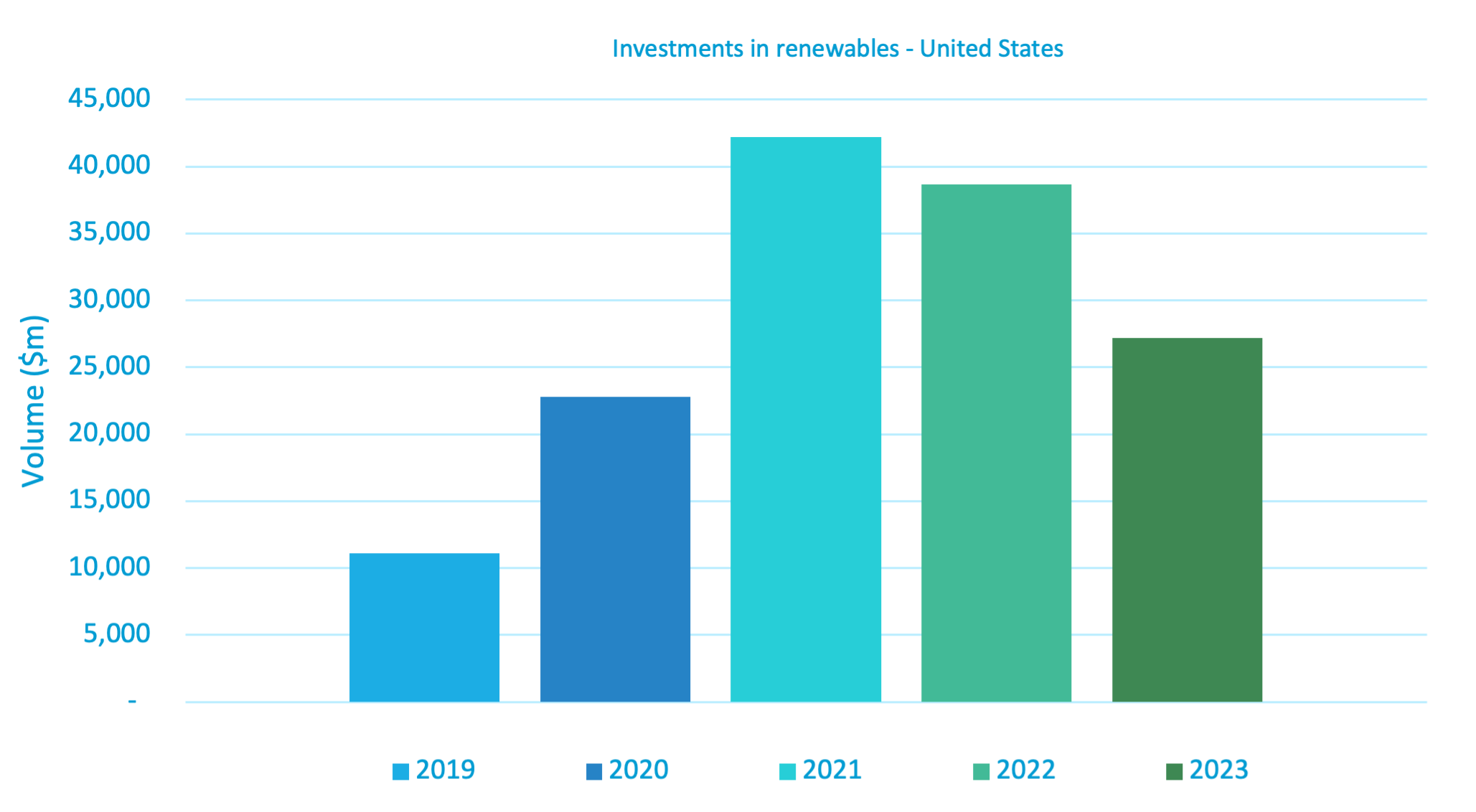

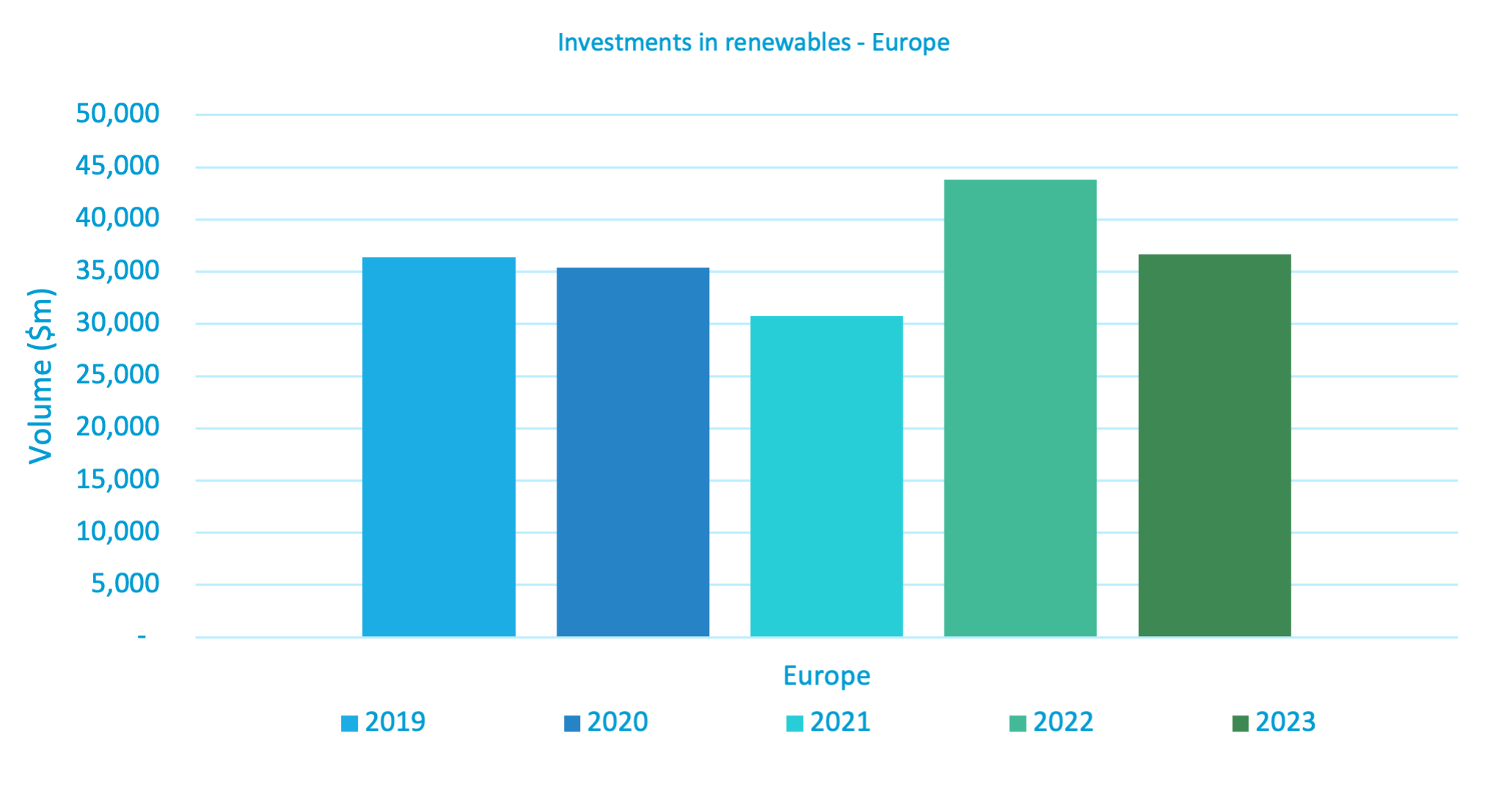

Proximo data highlight the surge in investment since 2019, with North America the second most dynamic market worldwide after Europe. The US alone saw an increase in investments from $11.1 billion in 2019 to $38.6 billion in 2022. The standout year was 2021, when the US recorded $42.1 billion of renewables investments, accounting for 43.4% of the global total of $99 billion that year.

That sharp increase in US volumes can be compared to Europe’s performance, which generally remained static over that period. It recorded small falls from 2019 to 2021, ending that year behind the US. That year looks a little like an aberration, with Europe pulling ahead in 2022 and 2023 to date. But the US, despite an uncertain political commitment to decarbonisation pre-2021, has essentially pulled level with Europe as a whole.

But that surge in investments has led to a transformation of the US energy landscape. According to the US Energy Information Administration (EIA), the share of renewable energy sources in the US electricity mix reached a record 22% in 2022, with wind leading the charge, closely followed by hydro and solar energy. This transformation occurred alongside a decline in coal's share, which fell to 19% in 2022. Natural gas remains dominant, with a 39.4% share in energy generation.

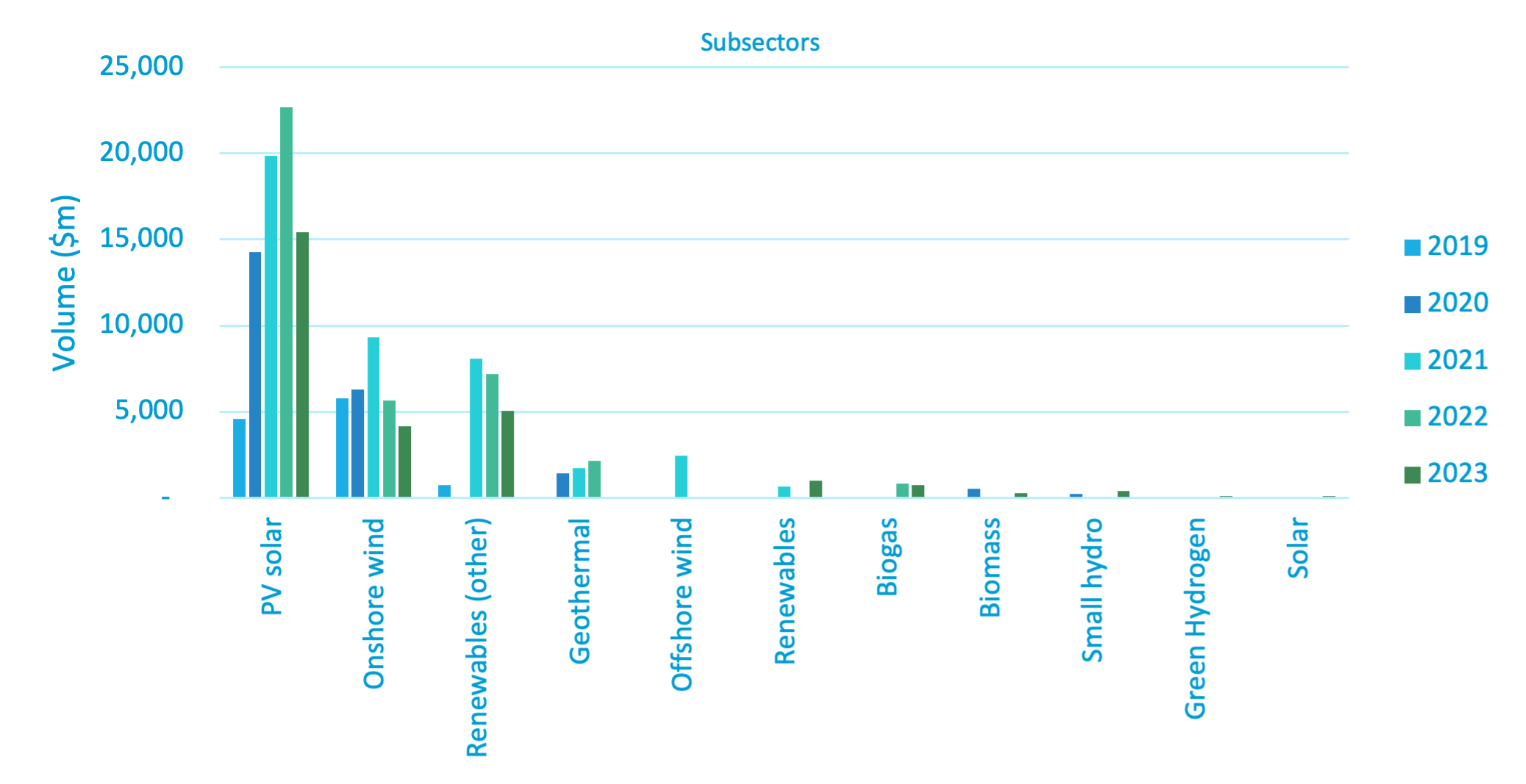

Solar energy investments, in particular, have risen sharply over the past four years, surging from $4.5 billion in 2019 to $22.6 billion in 2022, and almost compensated for a fall that year in onshore wind volumes. It is possible that 2023 might set new records, with $15.4 billion already invested in the first three quarters of the year, and some big-ticket financings on course to close before the end of 2023.

The US benefits from a strong bench of independent power producers (IPPs), some of them with roots in the conventional power sector, who have continued to drive improvements to the process of developing and financing renewables additions. One IPP, for instance, Invenergy, has on its own closed on a total of $6.8 billion since 2019.

The 2022 Inflation Reduction Act (IRA) allocates $500 billion to stimulate clean energy, reduce healthcare costs, and bolster tax revenues, of which $400 billion has been allocated directly towards clean energy. That funding comprises tax incentives, grants, and loan guarantees, focusing on clean electricity and transmission, but followed closely by clean transportation, including electric vehicle incentives.

It is not clear the extent to which the IRA was a direct response to the dip in activity in 2022, given that project finance activity is likely to lag policy advances. But 2023’s volumes so far look more respectable than supercharged, and it is possible that 2024 could be the year the boost truly kicks in.

In electric vehicles (EVs), there is still a strong debate as to whether project finance activity is even likely to be the yardstick by which success is measured, given that procuring vehicles and infrastructure may be best accomplished using different financial products. But the general picture is of a surge in demand for electrical vehicles.

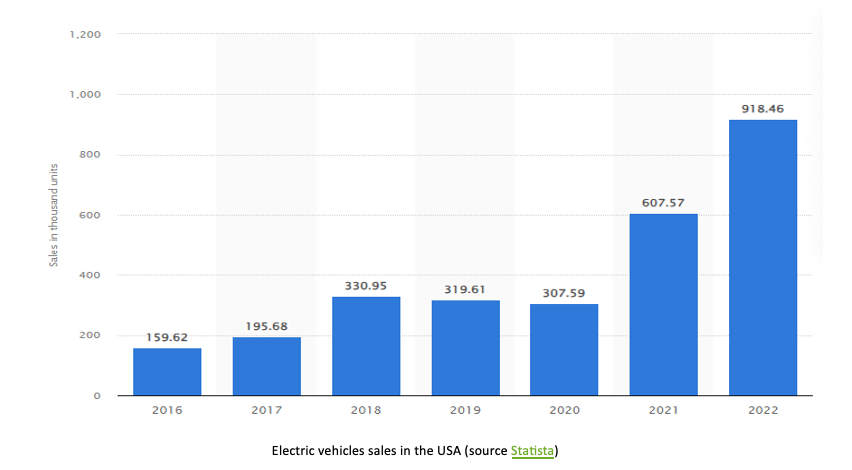

High gasoline prices in the US (at least compared to historical domestic levels) are making EVs much more appealing to consumers. Recent data from the EIA show that the US recorded 918,460 in sales of EVs, equivalent to 7.1% of all vehicle sales, in 2022.

The EIA predicts that the US is likely to record a 60% increase in sales in 2023, and here the impact of the IRA will be much more clear. The act capped the price at which EVs qualify for tax credits, prompting EV manufacturers to maintain competitive pricing even as battery costs have increased. But even as charging networks in Europe attract support from project finance lenders, the US is still playing catch-up.

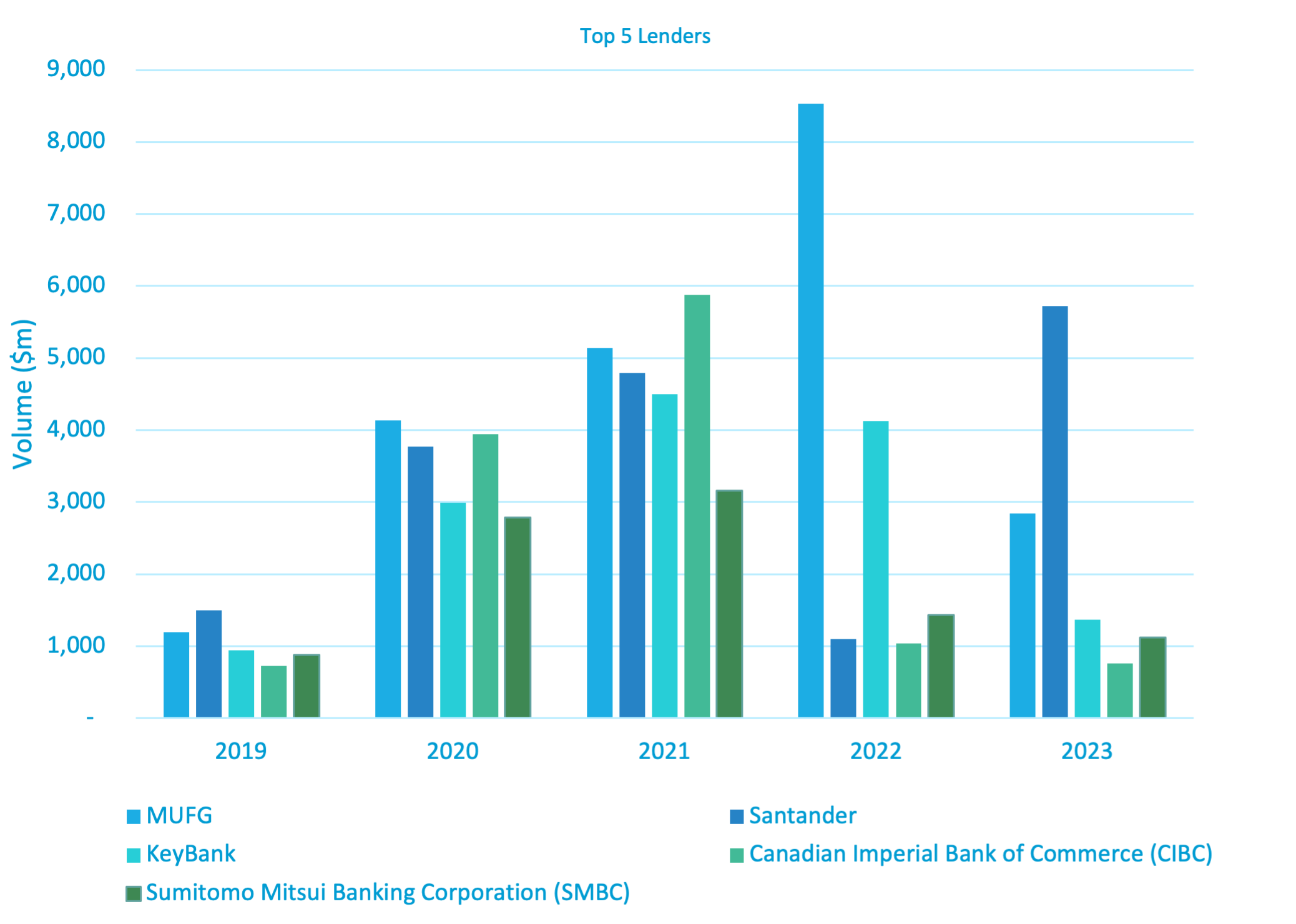

But the bank capacity is probably available, from a combination of domestic, regional and international lenders. MUFG stands as the most active lender, with a total of $21.8 billion mobilised since 2019, including a remarkable peak of over $8.5 billion in 2021. But Santander has also emerged as a significant lender, contributing $5.7 billion in 2023 alone. KeyBank, which has shrugged off the issues faced by US lenders, CIBC, which has grown its franchise impressively since 2019, and SMBC complete the list of top lenders.

The Proximo perspective

Where next for the US power finance market? Project finance lenders appear to be most comfortable mobilising large amounts of debt for proven technologies and familiar sponsors with deep pockets. For now, the US Department of Energy’s Loan Program Office is doing most of the heavy lifting in testing whether newer technologies are bankable, not commercial banks.

But the US project finance market is still ready to innovate. Recent financings for transferable tax credits, a new feature of the US tax incentive market introduced under the IRA, show a community ready to respond to policy innovations. And the institutional debt market does look welcoming to renewable energy issuers, despite recent higher debt costs. For now US leadership in renewables investment looks assured.